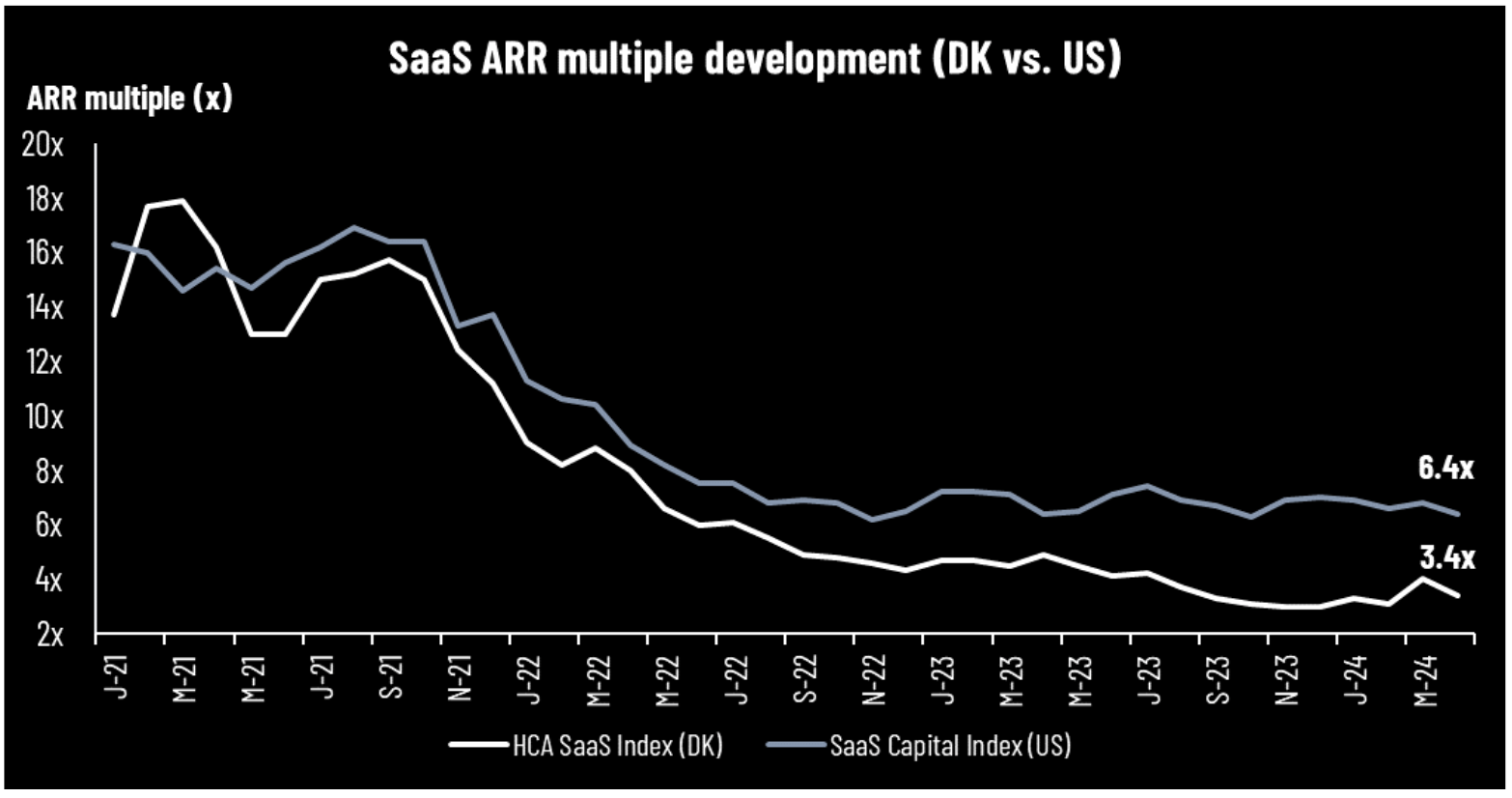

Source: HC Andersen Capital and The SaaS Capital Index

As we recently published our SaaS sector report on 30 April 2024, most of this newsletter will center around the news and findings from this report which you can read here. Since this came out, however, we have updated multiples from the US/global and Danish SaaS sectors, showing that the median ARR multiple (latest reported) declined in April to 6.4x (US) and 3.4x (DK).

A key theme, both over the recent year and in our SaaS sector report, has been the ongoing wave of acquisitions and delistings in the Danish SaaS sector. This was also the case in late April, as Relesys received a binding agreement on all shares from the private equity fund, Copilot Capital Limited. The acquisition price is DKK 6.60 per share, corresponding to approx. 5.1x EV/ARR (2023) and 3.7x EV/ARR (2024E) based on guidance midrange, i.e. significant above the current median ARR valuation multiple for the Danish SaaS sector. While observing delistings in Denmark, the US SaaS sector of listed companies welcomed Rubrik, as Rubrik made an IPO in late April. Currently, the Rubrik share trades slightly above its IPO price even though the share had a good start shortly after the IPO.

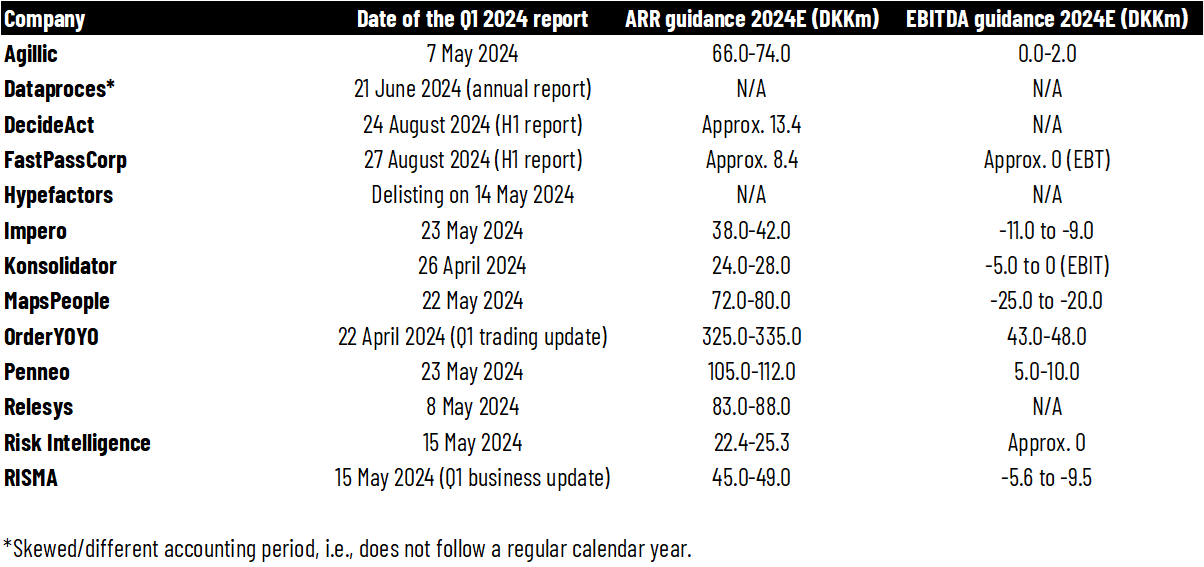

Looking ahead, many of the Danish SaaS companies will report their Q1 2024 results in May. We have already seen the first, which we will cover in more details in our May newsletter. In this newsletter, we provide an overview of when the Danish SaaS companies report.

So far, what we have seen from the US SaaS Q1 2024 reporting season has been mixed. Looking at the three hyperscalers (Azure, AWS, and Google Cloud), the messages have been positive, as they see meaningful acceleration. Amazon’s CEO Andy Jassy commented positively on the AWS segment: “[…] companies have largely completed the lion’s share of their cost optimization and turned their attention to newer initiatives”. According to Clouded Judgement (Jamin Ball), however, this optimism is not seen in the pure-play SaaS companies yet. Only ~20% of the US SaaS companies have reported Q1 results, but 2/3 of the companies that are guiding for Q2 had guidance below the analyst consensus. Thus, there seems to be some lag from the hyperscalers’ positive sentiment to the rest of the software universe.

Overview of reporting date for the Danish SaaS Q1 earnings season

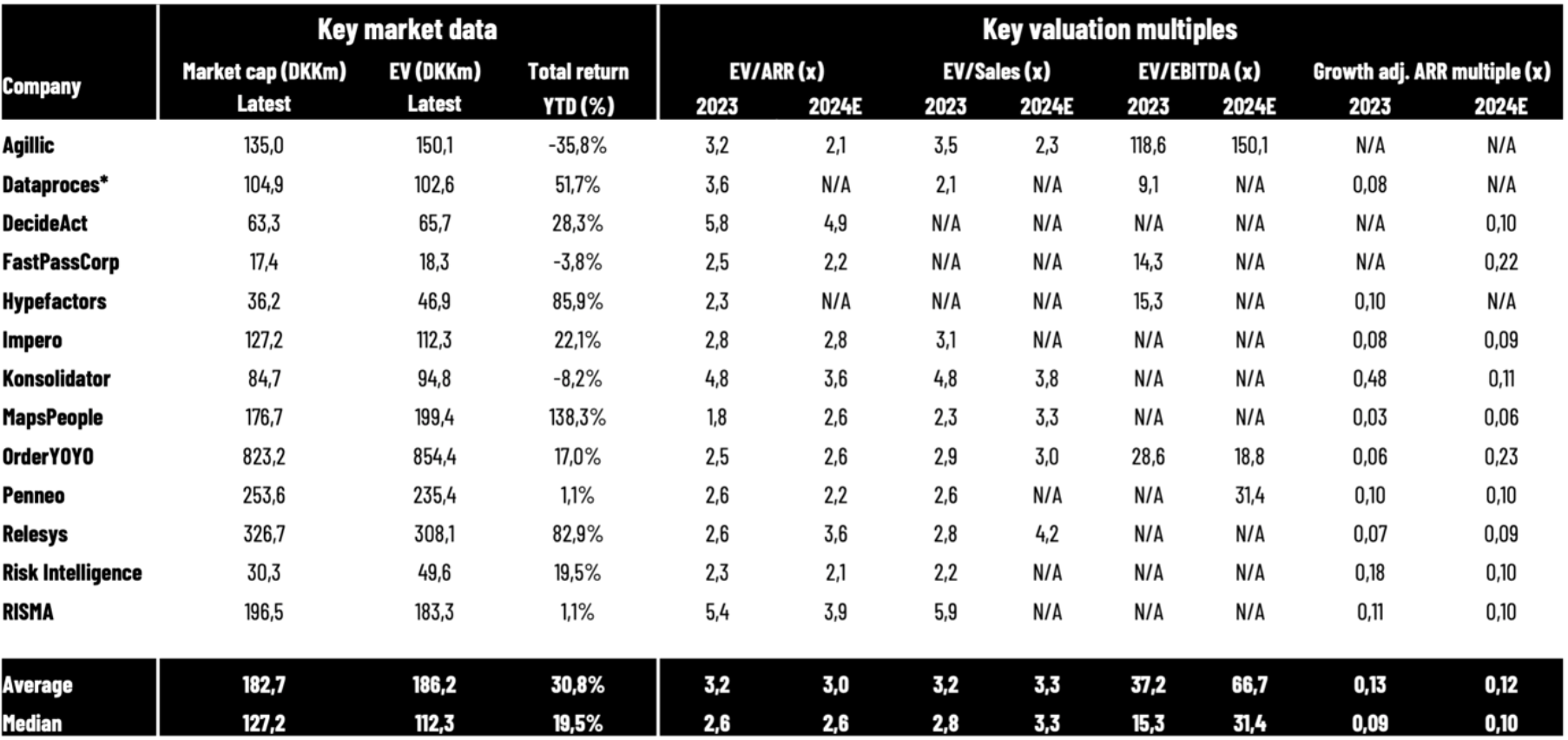

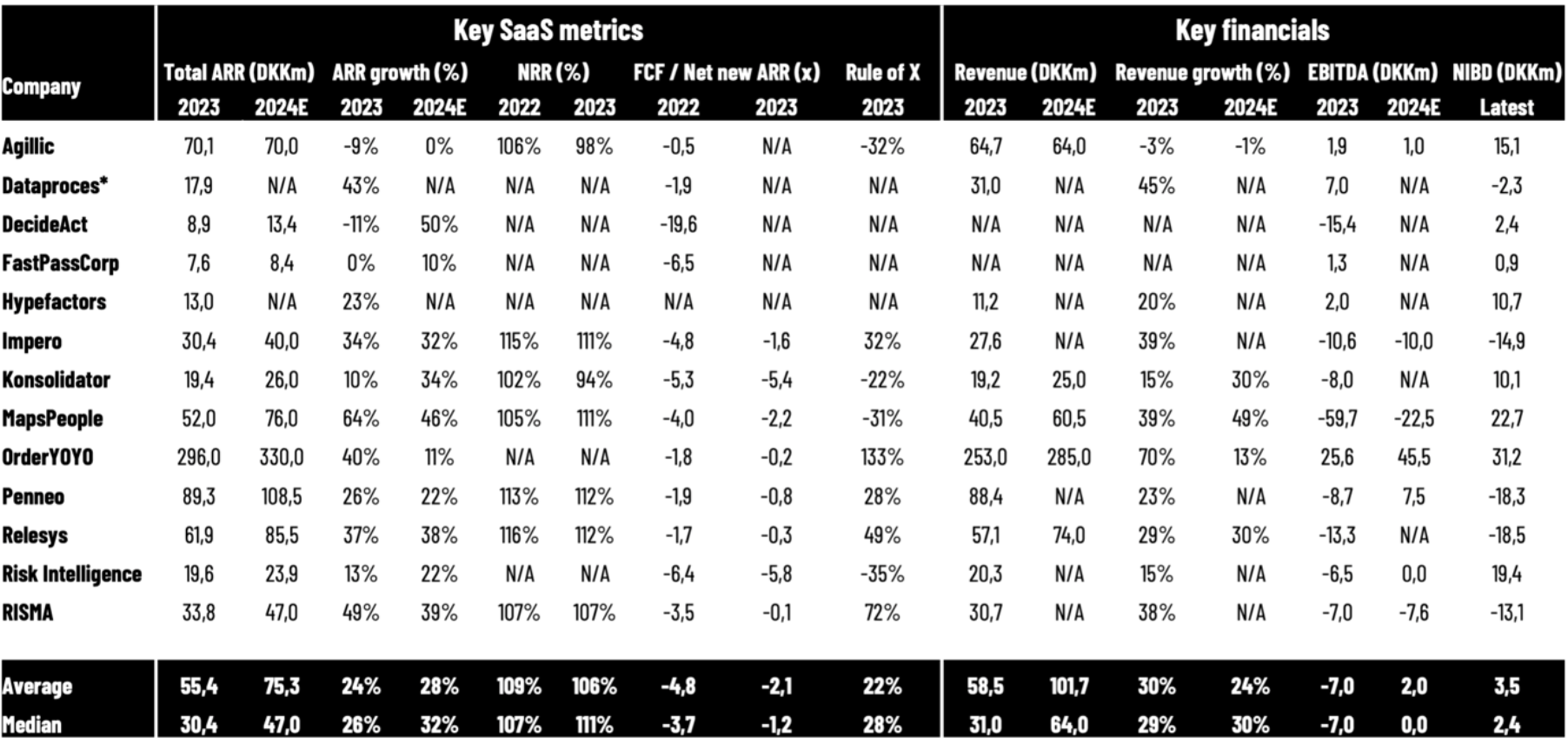

Overview of key metrics for Danish SaaS companies

We have collected data from 13 listed Danish SaaS companies. The overview will be updated on an ongoing basis. Market capitalizations are latest updated on 30 April 2024. Read the note below the tables for more detailed information.

Note: The table above summarizes key market data, key valuation multiples, key SaaS metrics, and key financials for Danish-listed SaaS companies reporting ARR (some software companies such as cBrain do not include ARR in their reporting and are not included). *Dataproces has a skewed/different accounting period than a regular calendar year. We apply the companies’ reported SaaS metrics, however, there are differences in the reporting methodologies, as there are no regulations or standards yet. When applying 2024E for the companies, we are using the companies’ guidance ranges (midpoint). We apply OrderYOYO’s pro forma net revenue in this overview (app smart consolidated full year) for both valuation multiples and growth rates. FCF/Net new ARR (2022) is calculated by taking FCF (cash flow from operations minus CAPEX, primarily investments in intangible assets) and the net ARR increase by the end of 2022 compared to the end of 2021. Penneo adjusts its FCF/Net new ARR ratio by DKK 2.4m due to costs related to the listing on the Main Market. Taking these costs out, the ratio will decline from -1.9x to -1.7x. In the calculation of net-interest-bearing debt (NIBD) for the companies in 2022, we have applied interest-bearing debt (including leasing liabilities) minus cash. This implies that negative values are companies with more cash than interest-bearing debt on their balance sheet. We apply the latest reported NIBD (for most companies) and market capitalizations from 31 December 2023 in our calculations of Enterprise Value multiples for 2023, and market capitalizations from 30 April 2024 for 2024E. MapsPeople’s net revenue retention rate (NRR) is based on MapsIndoors. All data is collected manually from reports, and we cannot guarantee the correctness of all data. Source: HC Andersen Capital and company reports.

Appendix: We are fully aware that no SaaS companies have similar business models or similar reporting standards, as there are no regulated standards yet for SaaS metrics such as ARR, net revenue retention rate, etc. Nevertheless, we do not have any public information to align all metrics, implying that we must use the metrics reported by the companies in their annual reports. Consequently, our information and benchmark data should be assessed carefully before making any conclusions or decisions. That said, we are active in a working group that provides recommendations for how to measure and report the metrics to investors in the most appropriate way.

The HCA SaaS Index: Our HCA SaaS Index is inspired by the US-based The SaaS Capital Index, which tracks the median ARR (latest reported annualized current run-rate revenue) multiple across US-listed B2B software companies based on their market capitalizations by the end of the month. This implies that there are timing variations in the latest reported ARR, and the multiples do not account for differences in cash position and debt structure. Please be aware that the US-listed companies are typically significantly larger companies with a global presence than the companies that we are tracking in Denmark. Despite the ongoing focus on profitability as well as capital efficiency and not only growth, SaaS companies are still valued on a multiple of their ARR or revenue. Currently, this is the most relevant multiple to compare across the sector since most SaaS companies are not profitable yet.

Disclaimer: HC Andersen Capital receives payment from some of the mentioned SaaS companies (Agillic, Impero, MapsPeople, OrderYOYO, and Penneo) for a Digital IR/Corporate Visibility subscription agreement. All content in this newsletter is only for informational purposes. HC Andersen Capital cannot guarantee the correctness of all data in this newsletter.